I am going to try to answer them as best as possible...I think some graphics will be necessary...

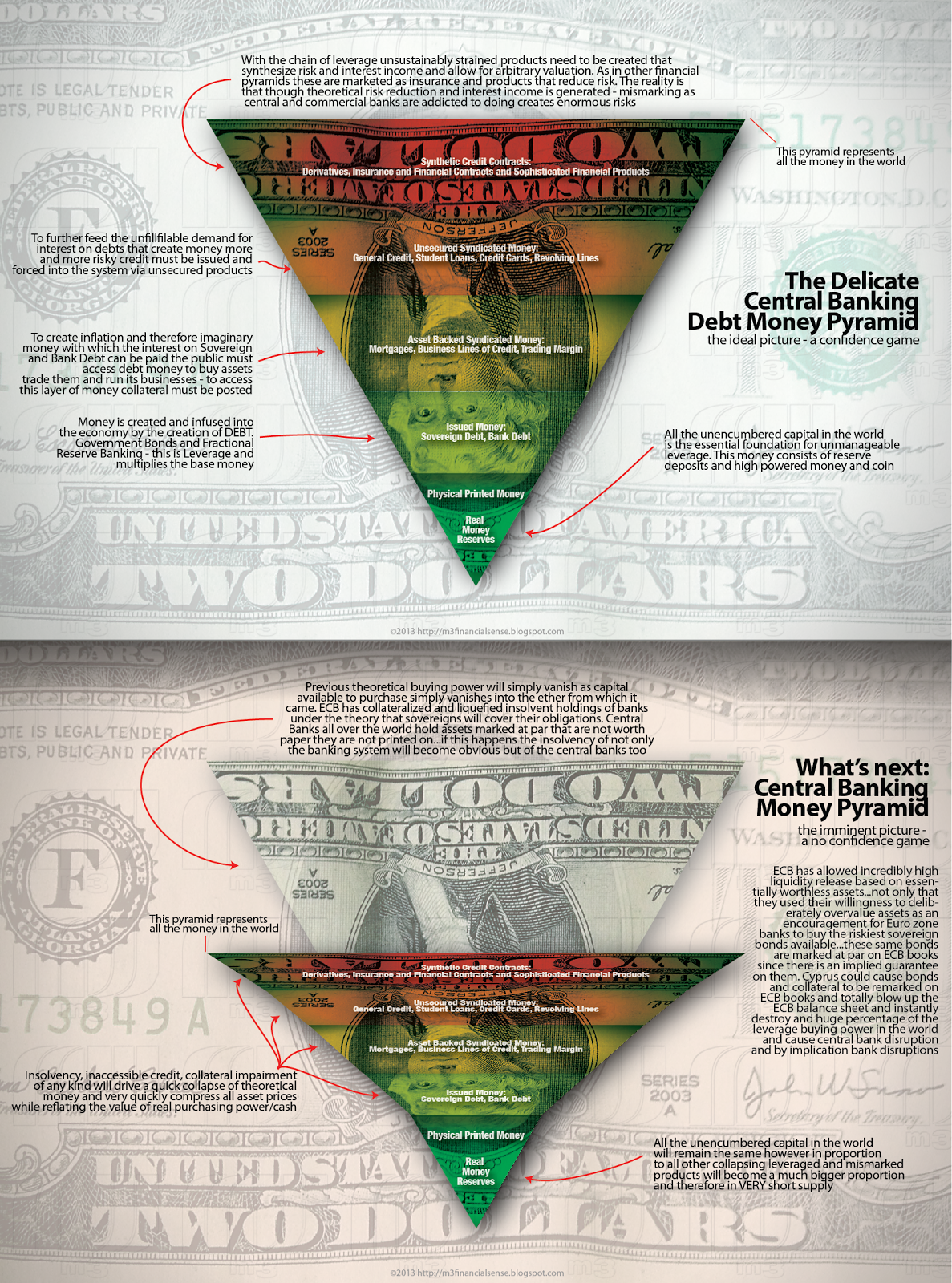

As you can see above, I show no actual assets on this pyramid. That is because almost every asset in the world is collateral for some sort of debt. The fact is that though you may think you own your home when it is paid off, the government has already pledged it in some from or another in order to create new credit money.

Now to the questions:

- The ECB is the defacto regulator for all EURO banks. Cyprus banks have been insolvent for years, yet its only NOW that we find out that they were allowed to store nearly all of their reserves in Greek bonds...how could this be possible?

- Since Greek (among others) bonds imploded years ago, just who is the bigger problem? the regulator who allowed concentrated investments in them? The regulator that allowed them to be held on books, used as collateral and itself leveraged with the pretense of solvency?

Obviously, any astute foreign nationals with money in a Cyprus bank must have been withdrawing large amounts of money recently in order to create the present condition that the ECB finds so contradictory and repugnant and that it had to be handled in the most ridiculous and inept way they have chosen. What else has really changed in the last months that should change the ECB's policy so drastically? Several years ago Greek bonds were actually worth less than recently and ECB did not force Cyprus to steal money from its depositors. They obviously have done so now because the EURO system is riddled with similar problems and the ECB is for all intents and purposes, insolvent.

We need to remember that ECB is holding vast amounts of worthless bonds as collateral, not just Greek, but Spanish and Italian, Latvian and Belgian etc…they have sustained the pretense of things improving by encouraging banks to take tremendous risks and purchase relatively high yielding bonds with the benefit of high collateralization rates with ECB…when sovereign guarantees are meaningless ECB will be forced to mark them properly rather than magically.

- Why is ECB trying so hard to resist the Greek style "close your eyes and do anything" approach and say anything PR campaign?

ECB clearly has fear of much bigger problems and needs to manage its behaviour now in such a way as to not have to roll over for the other 15 insolvent EURO nations when they can no longer suppress them. Spain and Italy make Cyprus look like an ant on an ant hill compared to the giant Dung Beetles waiting to emerge from their burrows, since a Cypriot national default would render the ECB immediately insolvent and require all plus some of their reserves.

- Just how much collateral is the ECB holding on its books at par that is really @ 0?

More than I can count for sure…I would like to know this answer specifically however…

- Just what is the theft, I mean haircut, ahemm - levy and what does it mean? Who does it really effect? How long are funds impaired?

The funny thing about this haircut issue is that its really not as advertised. As I get ready to post this, a 40% haircut has been agreed to and that is exceeding even my worst expectations. But if that was the end of the story that would be bad enough, but it is not.

If you have 1 million Euros in Laiki Bank, 100,000 will be paid to an account at a supposedly solvent bank. The remaining 900,000 will be held in a “bad” bank…360,000 will be deducted leaving 540,000 which you will not be able to access till the bank is liquidated…at which point you will likely find out that you will get 10 to 30% of the remaining amount - IN FIVE YEARS!!!

So, the advertised 40% haircut is likely really only going to give you 200,000 to 250,000 euros back. If you happen to be an employer in Cyprus, you are not anymore. And while its nice that all the individuals with less than 100,000 in their account will be whole…they likely will be out of a job. Politicians will of course. demonstrate that they saved the voters from loss…and though those voters will be out of a job because the bulge bracket employers are no longer…the Cypriot leaders will blame Germany for that little issue. hmmmm

- How is JP Morgan involved?

Though, as far as I can yet see, JP Morgan is not involved with the Cyprus debacle directly. However, they 80 trillion of mismarked securities are a symptom of the the Central Banking system and Banking System run amok. This is the exact problem that has encouraged the top levels on the chart above and which is enabling the ECB and many other central banks and banks to operate as if they are solvent when they are absolutely the opposite. JP Morgan is just the poster boy and the example…ohhh, and by the way, totally insolvent.

- Cyprus is so small - does it really matter?

A Cypriot national default would render the ECB immediately insolvent and require all plus some of their reserves…and that matters a great deal if Van RUMPy and BarRUFFo would like to keep their cushy corner offices.

- What is the architecture of this problem?

One thing of note, when Ben BURNanke was hased if American’s would be hit with a similar crisis and haircuts, he neglected to answer the question at all, and instead said that “Since the worst of the economic crisis in 2008, the FDIC has protected every account and not one person has lost a single dollar"…I hope you don’t mind if I read between the lines.